When Can I Draw From My Tsp

One of the questions that Federal Employees often ask us is how they tin convert some of their Thrift Savings Programme (TSP) dollars into the ROTH component of the TSP.

As a Federal Employee or member of the armed services, there are and then many advantages to actively participating in the TSP. Amid them is that you lot tin can select how you lot want your contributions treated for federal income tax purposes. There are two choices: Traditional and ROTH.

Traditional vs. ROTH Contributions

Traditional contributions are "pre-tax" contributions and designed for tax-deferred treatment. Pregnant, the monies that you lot contribute in this capacity are not taxed until y'all withdraw them. Monies in your traditional component of the TSP are subject to Required Minimum Distributions (RMDs). This ways that when yous reach age 70 ane/2 you volition have to have a calculated amount of monies out of this investment vehicle. If you don't, you risk incredibly pregnant fines for not doing so.

Conversely, you lot can too make contributions to the ROTH component of your TSP which are after-tax. Meaning, the monies that y'all put in are taxed today at your current charge per unit then that when you withdraw them later in retirement, you can practise so tax-costless providing that you lot satisfy the Internal Revenue Services (IRS) requirements. ROTH investment contributions are not subject field to RMDs considering you already paid tax on the money you lot put in.

In the world of private investments, outside of the TSP, a popular strategy was to accept monies previously placed in a Traditional Individual Retirement Account and catechumen them to a ROTH Individual Retirement Account. Through a strategy chosen a Roth Conversion, investors took the funds from the Traditional IRA and converted them to the ROTH IRA, and then that they could pay taxes on the monies at their current rate and have reward of the "revenue enhancement-free" status of these accounts earmarked for later in life.

Converting a Traditional IRA to a ROTH IRA

The TSP does not allow for ROTH conversions.

The TSP will allow you to change the taxation status of your contributions from Traditional to ROTH which will touch contributions moving frontward. However, the TSP does not allow for retroactive changes; you cannot change the monies you already allocated into the traditional revenue enhancement status (tax-deferred) to the ROTH status (taxation-free).

Yous can change your TSP contributions from tax-deferred to the ROTH by logging into your TSP account online and selecting to do so.

What options do you lot have if you are younger than 59 1/ii? Well, not many when information technology comes to converting funds from your traditional TSP to a ROTH. However, if you lot are separated from service or over age 59 1/two at that place is a unique planning method you could explore.

Transferring TSP to IRA

If you are separated from service or you take reached age 59 1/2 you lot tin transfer, TRANSFER – NEVER Curlicue OVER, some of your TSP funds into an Individual Retirement Account. Caution: Strike the word "Rollover" from your vocabulary and be leery of anyone who uses this term with you. Rollovers are not bad only you have to understand how they piece of work. They are not synonymous with the give-and-take "transfer." When you scroll over an account, the agency — in this case, the TSP part — takes your funds and withholds 20%. They ship those withholdings to the IRS. Then, the TSP role sends you the eighty% residuum of what y'all requested. Inside sixty days, you must put 100% of those funds (including the 20% that now sits with the IRS) into a retirement account.

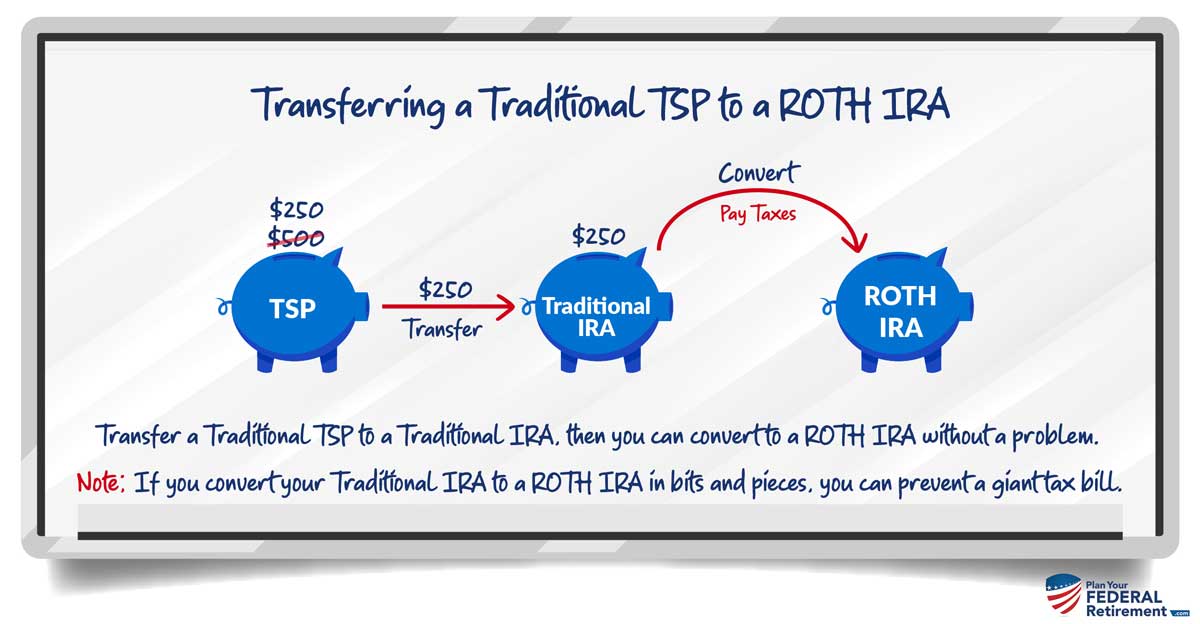

Transferring Traditional TSP into a ROTH

If your end goal is to take all or a portion of your traditional TSP and motility it into a ROTH, here is a strategy that you can consider after properly weighing the revenue enhancement consequences and understanding the operational order.

If y'all are separated from service or accept reached age 59 1/2, you lot are allowed to make an in-service withdraw or distribution from your TSP. You tin transfer the appropriate portion into a traditional IRA. One time the funds are in a traditional IRA, you tin can convert the funds to a ROTH IRA. Keep reading about taxes below. In this process, at that place are 3 accounts open: TSP, IRA, and ROTH IRA.

At present, before you get too excited and want to convert 100% of your monies into a revenue enhancement-free account, recall, the money that you are converting is taxable when you convert information technology. As a helpful financial planning tip, y'all do non have to convert all at once. Consider staging the conversion over several years or when it is most tax advantageous to do then.

When you begin to take your FERS Pension and Social Security, those income taxes are taxable. Could you choose a fourth dimension period Before you lot draw those to make a conversion? If ane spouse retires sooner than the other and you experienced a decline in your tax status, could yous do it then? If you lot experience a turn down in the markets and anticipate that in time those investments will become back upwardly, is that a good time to convert? Y'all want to carefully conduct a tax analysis to determine what your taxation bracket is and the nigh advantageous amount to convert to a ROTH.

No "Undo" Button

Please call back that under the Tax Cuts and Chore Act in that location is no longer an "undo" button on the ROTH Conversion. Once you catechumen those funds, there is no going back. Y'all may want to consider waiting until the Fall time period to acquit a ROTH Conversion just so you have time to most accurately anticipate your taxable earnings for that year.

Happy Planning!

Source: https://plan-your-federal-retirement.com/how-can-i-convert-some-of-my-tsp-dollars-into-my-roth/

Posted by: grantficame.blogspot.com

0 Response to "When Can I Draw From My Tsp"

Post a Comment